How to Know If a Home Loan Balance Transfer Is Worth It in 2026 | Complete Guide

Many homeowners continue paying higher home loan interest rates without realizing they may be able to reduce their monthly EMI and overall borrowing cost by switching to another lender. A home loan balance transfer can be a smart financial move, but it is not the right choice for everyone.

If you’re considering switching your existing loan, our Home Loan Balance Transfer in Bangalore service explains the complete process, eligibility, and benefits.

Before transferring your loan, it’s important to evaluate the potential savings, associated costs, remaining loan tenure, and your financial goals. This guide explains when a balance transfer makes sense, how to calculate the benefits, and the key factors you should consider in 2026.

What is a Home Loan Balance Transfer?

A home loan balance transfer is the process of moving your outstanding home loan from your current lender to another lender offering more favorable loan terms. The new lender repays the outstanding balance to your existing lender, and you continue repaying the loan under the new agreement.Home loan lending and banking practices in India are regulated by the Reserve Bank of India (RBI).

Borrowers generally choose this option to:

- Lower their interest rate

- Reduce monthly EMI

- Save on total interest payable

- Access a top-up loan

- Improve repayment flexibility

Why Do People Transfer Their Home Loans?

Interest rates change over time, and lenders frequently introduce new loan products to attract borrowers. If your existing loan carries a higher rate than current market offerings, a balance transfer may help reduce long-term borrowing costs.If you’re exploring financing options beyond a balance transfer, visit our Home Loan Services in Bangalore page to understand the different home loan solutions available.

Common reasons include:

- Lower interest rates

- Better customer service

- Flexible repayment options

- Additional loan facilities

- Improved digital banking services

When is a Home Loan Balance Transfer Worth It?

A balance transfer can be beneficial in the following situations.

1. Your Current Interest Rate is Higher

If your existing home loan interest rate is significantly higher than rates available from other lenders, switching may reduce your total repayment amount.

For example, a reduction of even 0.50% to 1.00% over a long repayment period can result in meaningful savings.

2. You Have a Large Outstanding Loan Amount

The greater your remaining loan balance, the more potential you have to save through a lower interest rate.

Borrowers with only a small balance remaining may not recover the transfer costs.

3. Your Loan Tenure is Still Long

Balance transfers usually provide the greatest benefit during the early years of the loan because a larger portion of your EMI goes toward interest.

If only a few years remain, the savings may be limited.

4. Your Credit Profile Has Improved

If your income has increased or your repayment history has remained strong since taking the original loan, you may qualify for more competitive loan terms.Salaried professionals looking for competitive home loan options can also explore our Home Loan for Salaried Employees in Bangalore service.

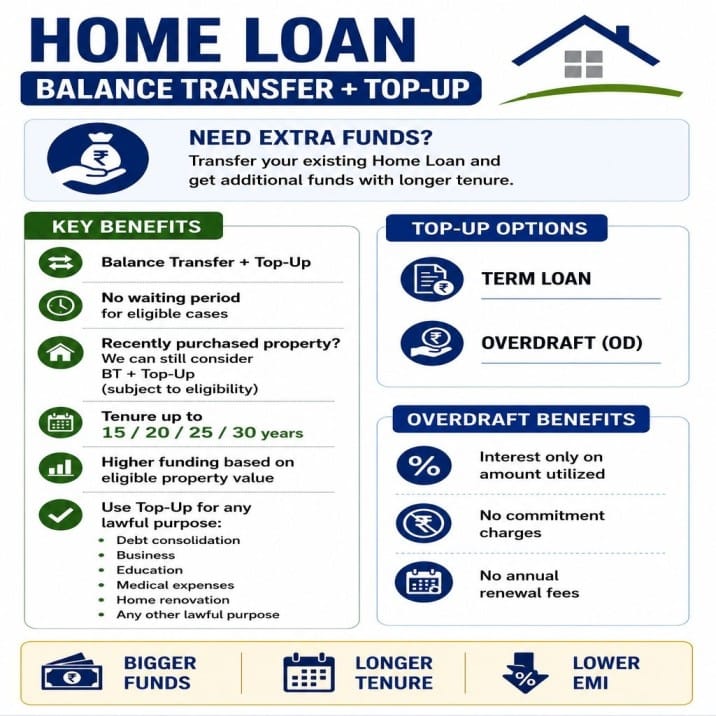

5. You Need a Top-Up Loan

Many lenders offer top-up loans along with balance transfers, providing additional funds for:

- Home renovation

- Education

- Medical expenses

- Business expansion

- Personal financial requirements

When a Balance Transfer Might Not Be Beneficial

A balance transfer may not provide enough benefit if:

- Only a small loan amount remains.

- The remaining loan tenure is short.

- Processing fees are too high.

- Legal and valuation charges outweigh potential savings.

- The interest rate difference is minimal.

- You have repayment issues affecting eligibility.

Always compare the total savings with the overall transfer costs.

Costs to Consider Before Switching

Before transferring your loan, calculate the following expenses:

- Processing fees

- Legal verification charges

- Property valuation charges

- Documentation costs

- Administrative fees

- Any applicable foreclosure or prepayment charges (if any)

A transfer should only be considered if the projected savings exceed these costs.

How to Calculate Your Savings

Evaluate the following:

- Outstanding loan amount

- Existing interest rate

- Proposed interest rate

- Remaining tenure

- Monthly EMI

- Total interest payable

- Total transfer expenses

Comparing these figures helps determine whether the transfer will deliver genuine financial benefits.

Eligibility for a Home Loan Balance Transfer

Although requirements vary between lenders, applicants generally need:

- A stable income

- Good repayment history

- Satisfactory credit score

- Existing home loan with an outstanding balance

- Required income and property documents

- Information about housing finance institutions and the housing finance sector is available from the National Housing Bank (NHB).

Documents Typically Required

Prepare the following:

Identity Proof

- Aadhaar Card

- PAN Card

- Passport

- Driving Licence

Address Proof

- Aadhaar Card

- Utility Bill

- Passport

- Voter ID

Income Documents

For salaried applicants:

- Salary slips

- Bank statements

- Form 16

For self-employed applicants:

- Income Tax Returns

- Profit & Loss Statement

- Business Proof

- Bank Statements

Loan Documents

- Sanction Letter

- Loan Statement

- Foreclosure Statement

- Property Papers

- Before applying, review our Documents Required for a Home Loan in Bangalore checklist to ensure you have all the required paperwork.

Typical Errors to Avoid

During the transfer process, many borrowers commit preventable errors.

Steer clear of these:

Just comparing interest rates

Disregarding processing costs

Selecting an unnecessary extended tenure

Not figuring out the overall savings

Applying without verifying your eligibility

Disregarding the quality of client service

Tips Before Applying

To improve your chances of a successful balance transfer:

- Compare offers from multiple lenders.

- Check all applicable charges.

- Maintain a healthy credit profile.

- Keep documents ready.

- Understand all loan terms before signing.

Frequently Asked Questions

1. After a balance transfer, will my EMI decrease?

If the new lender offers a reduced interest rate or a different repayment plan, it can.

2. Can I transfer my loan multiple times?

While possible, frequent transfers may not always be financially beneficial due to processing costs.

3. Does a balance transfer affect my credit score?

Applying may result in a credit inquiry, but responsible repayment under the new loan generally supports a healthy credit profile.

4.Can I get a top-up loan with the transfer?

Many lenders offer this option, subject to eligibility and internal policies.

5. Are self-employed borrowers eligible for a balance transfer?

Yes, provided they fit the lender’s qualifying requirements, both self-employed and salaried candidates may apply.

Conclusion

A home loan balance transfer can be an effective way to lower borrowing costs and improve loan terms, but it should be based on careful evaluation rather than interest rate alone. Consider the outstanding balance, remaining tenure, transfer costs, and long-term savings before making a decision.

If the numbers work in your favor, switching lenders could help you save substantially over the life of your loan while improving your repayment flexibility.

If you need guidance comparing lenders or understanding the balance transfer process, feel free to contact us for expert assistance.